Audit Lowe Down – What are contract assets and contract liabilities that arise under the revenue accounting standards?

What are contract assets and contract liabilities that arise under the revenue accounting standards?

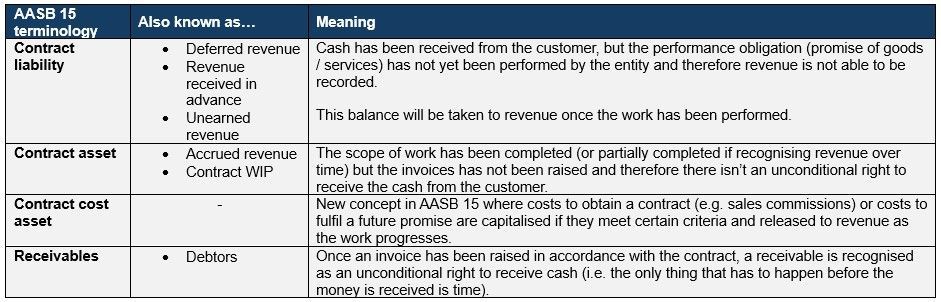

Deferred revenue, accrued revenue, revenue received in advance, contract assets, contract costs asset, contract liabilities and receivables are all line items we see in the balance sheet in relation to revenue. It can be confusing to understand what these terms mean and whether different words are being used for the same thing.

We have provided a guidance to these and similar terms to enable you to use them confidently and understand their meaning in a balance sheet.

Please do not hesitate to contact your Lowe Lippmann Relationship Partner if you wish to discuss any of these matters further.

Liability limited by a scheme approved under Professional Standards Legislation