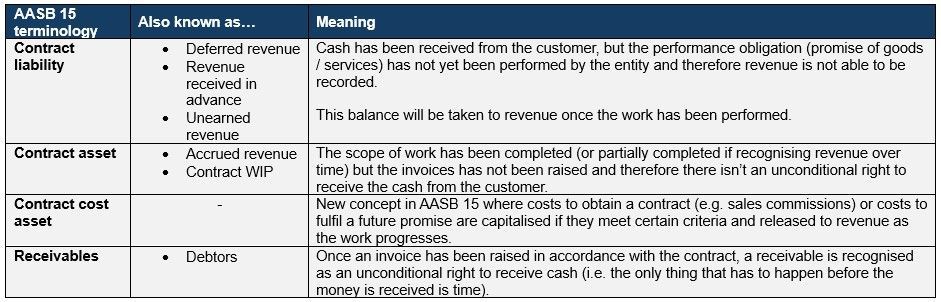

COVID-19 Commercial/Retail Landlords & Tenants Legislation Passed in Victoria

COVID-19 Commercial/Retail Landlords & Tenants Legislation Passed in VictoriaTwo weeks ago, the National Cabinet announced that property industry stakeholders were working on a National Cabinet Mandatory Code of Conduct ( the Code ), to allow each State and Territory to introduce legislation to implement leasing principles to help guide landlords and tenants impacted by the COVID-19 pandemic.

The Code introduced the following key points:

|

Victorian Legislation has now been PassedOn 24 April 2020, the Victorian Parliament passed the COVID-19 Omnibus (Emergency Measures) Act 2020 ( the Legislation ), which has introduced the leasing principles into law.

The Legislation is intended to come into operation on the day after it receives royal assent (ie. 24 April 2020), however the Legislation provides that regulations made under the Legislation may have retrospective effect to 29 March 2020 , being the date that the Prime Minister initially announced the rent relief measures which were subsequently included in the Code. It should be noted that both landlords and tenants will be bound to comply with the requirements of the Legislation from 29 March 2020, even though the Legislation was not passed until 24 April 2020. Therefore, any agreements reached between landlords and landlords under an "eligible lease" from 29 March 2020 should be reviewed to ensure those agreements comply with the Legislation.

At this time, we also understand that the leasing provisions relating to "eligible leases" will be repealed (cease having effect) in 6 months' time, which is the current time period used by all Government agencies for concessions relating to the COVID-19 pandemic |

What is an "eligible lease"?Retail leases and non-retail commercial leases or commercial licences may be considered "eligible leases".

Non-retail commercial leases are defined as leases which include premises that are let for the sole or predominant purpose of carrying on a business at the premises.

Under the Legislation, an "eligible lease" applies to tenants that are suffering financial stress or hardship that :

However, even where a tenant satisfies the two requirements above, some retail leases or non-retail commercial leases will not be an "eligible lease" , including circumstances where:

The three conditions here are drafted using the income tax terminology consistent with the concepts of "affiliates" and "connected entities" which are used to determine SME status by calculating the aggregated annual turnover of an entity and including group entities closely connected to it.

Also, the reference to a "certain threshold amount" (above) has not been defined in the Legislation, and further detail will be required in the regulations to identify with certainty the leases and tenants that will be excluded under the three conditions above. However, we consider that the three conditions above are drafted in such a way to be consistent with the Code, which provides that the $50 million turnover threshold is to apply in respect of retail corporate groups at the group level (rather than at the individual retail outlet level). |

The Scope of Regulations for Eligible LeasesThe Legislation does not explicitly detail rules of law to administer the practical issues which will potentially be experienced by landlords and tenants through the COVID-19 pandemic, instead it simply allows for the passage of subsequent Victorian regulations dealing with potential issues in relation to eligible leases.

The underlying policy objective of the Legislation is to provide a framework to assist the implementation of the good faith leasing principles outlined in the Code of Conduct.

The Legislation allows the (Victorian) Governor in Council to make regulations modifying rights and obligations in relation to "eligible leases" by:

|

Is Mediation Binding on the Parties?The Legislation empowers the (Victorian) Small Business Commission to:

The Legislation clarifies that landlords and tenants will be required to attend mediation as a precondition to commencing any other legal proceedings.

Early indications were that there would be a binding mediation process to resolve any disputes between landlords and tenants. However, the mediation will remain non-binding , and the mediator will not have power to make any binding determinations.. |

What is the impact for landlords and tenants?Although the Legislation does provides a general definition of what is considered an "eligible lease", further details are required to clarify the language used in relation to other entities associated with the tenant, which clearly may exclude certain tenancy arrangements from being an "eligible lease".

Effectively what the Legislation does is provide broad power to the (Victorian) Minister for Small Business to recommend regulations to implement the leasing principles set out in the Code and to respond to the COVID-19 pandemic. |

| Unfortunately at this time, this does not give landlords and tenants an acceptable level of certainty about their respective rights and obligations. However, the overriding principle of the Code is for both Tenants and Landlords to act in good faith.

We will continue to monitor the development of this topic, and provide further updates as and when regulations are issued and more information becomes available.

Please do not hesitate to contact your Lowe Lippmann Relationship Partner if you wish to discuss any of these matters further. |